Prevent risk.

Reward behavior.

Retain customers.

Keep your customers safe and up to date, and provide them with the most relevant service.

InfographicTELEMATICS SOLUTIONS

BEST PRACTICES

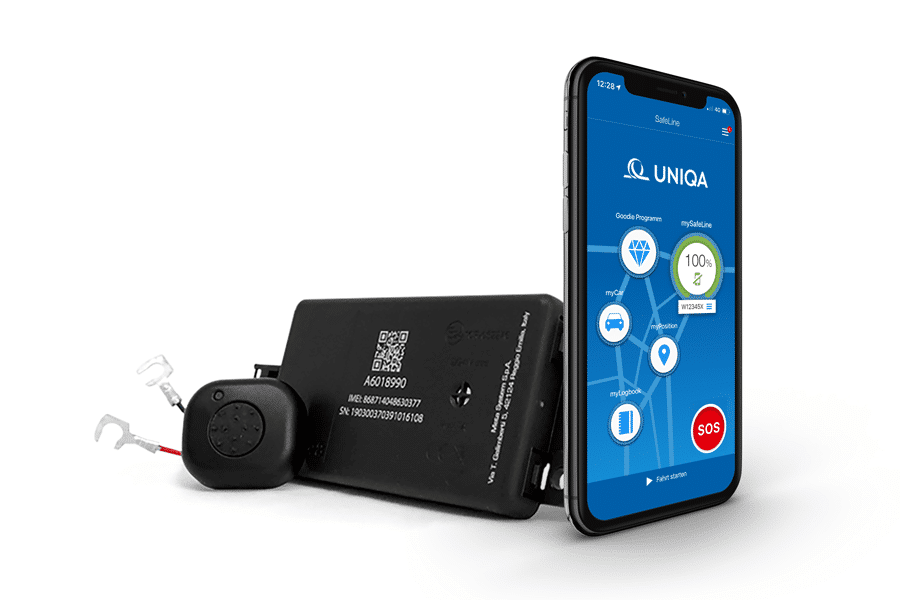

"SafeLine is a unique product that has attracted more than 80,000 customers."

"Passion, competence and commitment. An invaluable partnership!"

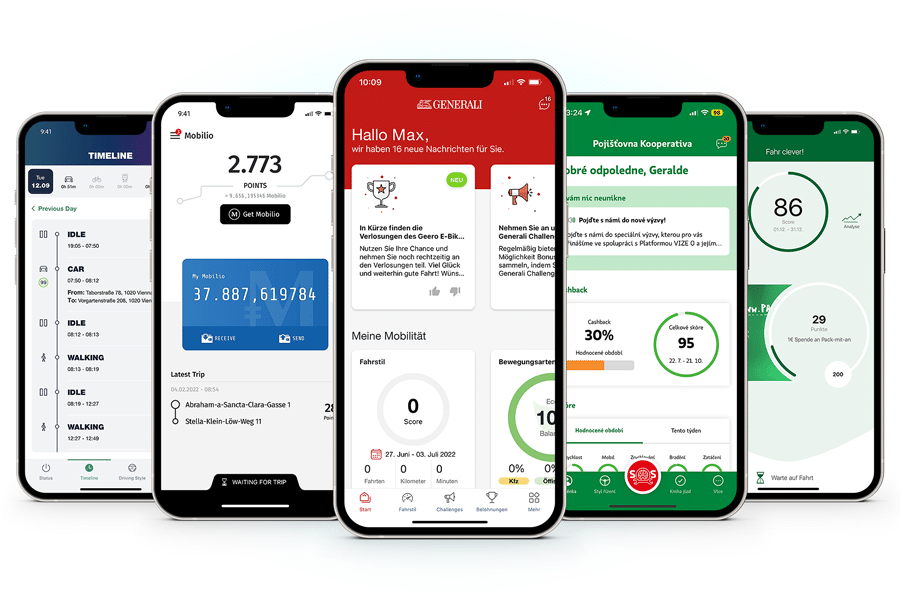

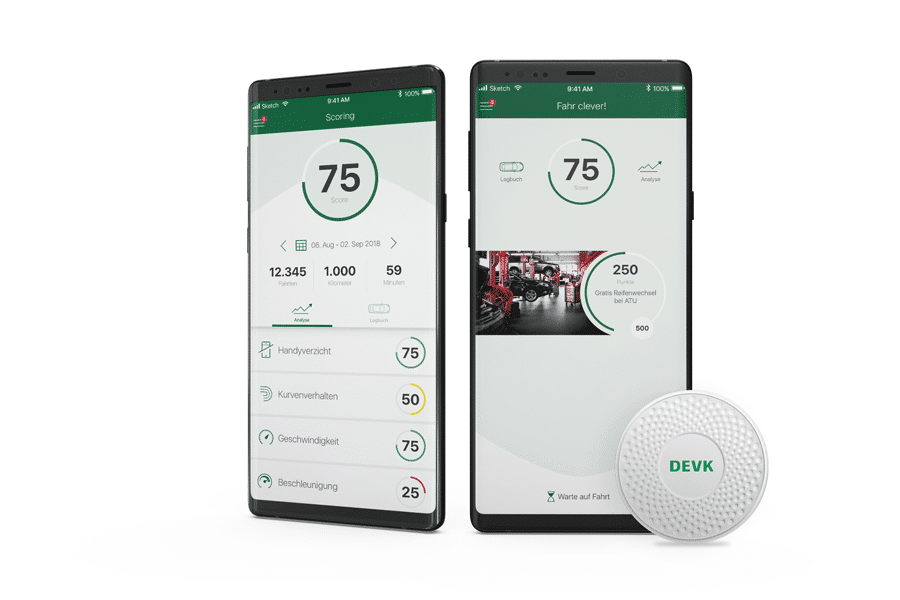

"Users of the "FahrClever!" App are delighted to be rewarded for cautious driving!"

"Awarded for outstanding achievements and industry leadership."

"Dolphin provides innovative technology to increase road safety."

"A winning partnership which helped to position ourselves internationally."

"Next generation insurance telematics with microservices" Case Study

"The Drive+ app increases road safety. Our customers love it!"

"Immediate help at the push of a button - The Generali Emergency App."

DOLPHIN IS A

FULL SERVICE AGENCY

Consulting

Strategy

Implementation

Analytics

Operations

Marketing

COMPANY

With solutions from Dolphin Technologies insurers evolve from writing policies and handling claims to become valuable partners in the life of their customers. Insurance companies can support people in real time in case of emergency, reward good behaviour, warn in time against potential risk, provide the right information at the right time, and support with smart solutions. Dolphin designs, develops, implements and operates scalable platforms, products, and services in the field of Telematics, Mobility, and Marketing Automation. Dolphin is an Austrian company, founded in 2001 and is repeatedly honoured nationally and internationally for excellence in innovation.

Gerald Aichholzer

Product Development-

Andreas Kössl

CCO -

Harald Trautsch

Co-Founder & CEO -

Thomas Pöschl

Co-Founder & COO -

Emanuel Altmann

Senior Development -

Georg Aschenfeld

Product Owner Implementation -

Oleksandr Baskakov

React Native Development

Robert Beisteiner

CISO - IT / Operations-

Mariya Belozyorova

Customer and Partner Manager -

Petra Bilikova

Scrum Master -

Sabine Binder-Blaha

Office Administration -

Annina Breitenecker

Graphic Design/UI/UX -

Denys Busiak

Quality Management -

Lukas Eichhorn

Quality Management -

Ersin Ergül

Product Owner SDK -

Dagmar Ilisson

Sales -

Emir Kazybaev

Data Engineer -

Lukas Kilian

Development -

Wolfgang Kilian-Löffler

Senior Account Management -

Florian Knoll

Android Development -

Bella Kocsis

Cloud Engineering -

Mirza Likic

React Native Development -

Alexandra Linecker

Quality Management -

Caroline Mayrhofer

Scrum Master -

Bence Laszlo Mindszenti

Quality Management -

Joao Victor Miranda

Data Science -

Markus Mühlbacher

Lead Backend Development -

Andrea Prosche

Customer Care -

Katharina Sallinger

Data Science -

Alena Santalainen

Customer & Market Management -

Victoria Scharf

Office Administration -

Peter Schüller

Data Science -

Demyan Shcheglov

Senior Development -

Pavlo Simakovych

Quality Management -

Dominik Stelzig

Content & Marketing -

Clemens Unterkofler

iOS Development -

Patrick Wohlfart

Installer Management / Sales